AI Decision Engines and Predictive Analytics in Finance

Written by Gokulram Krishnan

Financial institutions today face uncertainty, strong competition, regulatory pressure, and rising customer expectations. Traditional, reactive decision-making based on static rules and past reports is no longer enough to manage challenges like credit risk, fraud, customer retention, and personalized service at scale.

With the growing adoption of AI in financial services and advanced data analytics in finance, organizations are increasingly using predictive analytics in finance to anticipate risks and customer behavior before they occur.

Decision engines powered by AI-driven analytics and propensity prediction are transforming how institutions make decisions. By combining customer data with machine learning in financial services, organizations can move from simply analyzing past outcomes to predicting future ones and acting on them proactively.

Why Financial Institutions Need Predictive Decision Engines

Financial services generate vast amounts of data every day - transactions, customer interactions, digital behavior, and market signals. Yet many organizations still rely on rules-based systems and manual processes to guide decisions.

Predictive decision engines help institutions move beyond reactive decision-making by using data to anticipate outcomes and guide actions in advance.

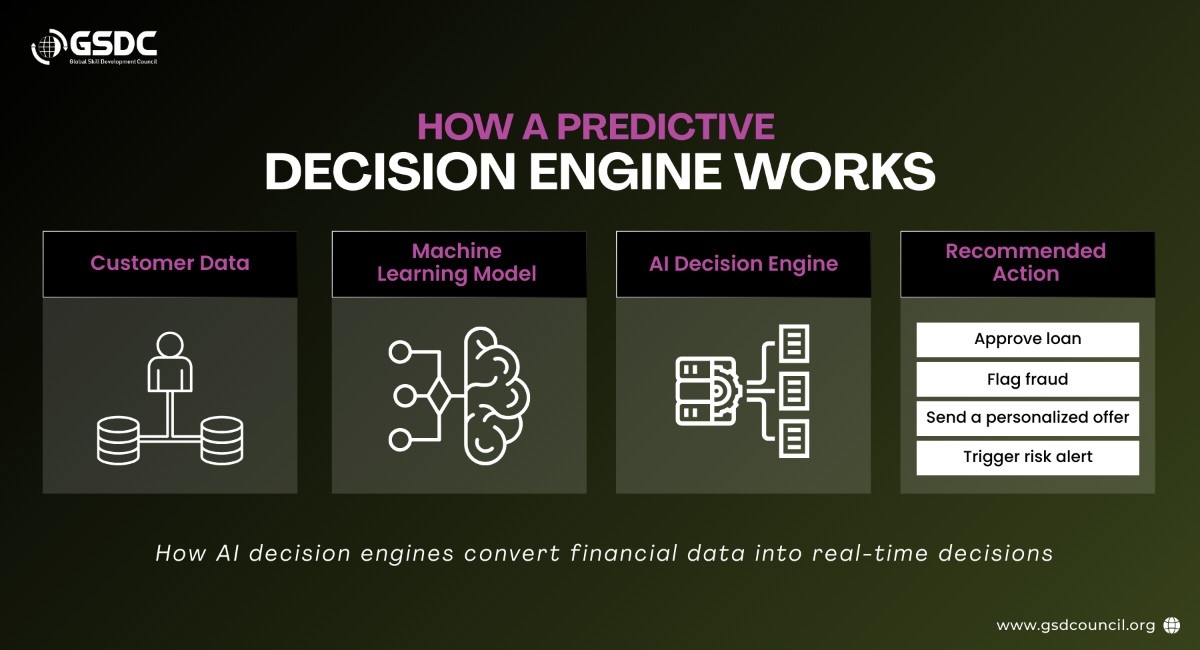

What Is a Predictive Decision Engine?

A predictive decision engine uses historical and real-time data to estimate what is likely to happen next and recommend the best action. For example, AI-powered decision engines analyze customer data to predict behavior and enable smarter financial decisions (Krishnan et al., 2025), which can signal default risk, fraud risk, or the likelihood that a customer will respond to an offer. These systems learn from new data, making decisions more accurate over time.

Decision engines supported by predictive analytics help institutions:

- Anticipate customer needs instead of reacting late

- Reduce risk through early detection of defaults or fraud

- Improve conversion with relevant, well-timed offers

- Automating operational decisions using AI decisioning

In a competitive market, the ability to predict what is likely to happen next is becoming a strategic advantage, not just a technical upgrade.

Understanding Propensity Prediction in Finance

Propensity prediction is a data-driven approach used by financial institutions to estimate how likely a customer is to take a specific action in the future. This helps organizations move from broad, generic actions to more targeted and proactive decision-making.

In financial services, propensity prediction can be used to assess the likelihood of customers:

- Accepting a new loan or credit card offer

- Defaulting on repayments

- Churning to a competitor

- Responding to a marketing campaign

- Filing a potentially fraudulent claim

These predictions are generated using historical customer data and machine learning models that learn patterns over time. The insights produced by propensity models enable organizations to focus resources where they are most likely to have an impact -improving outcomes for both customers and the business.

For example, instead of sending the same product offer to millions of customers, a bank can identify a smaller segment with a high propensity to convert, reducing marketing costs while increasing relevance and engagement.

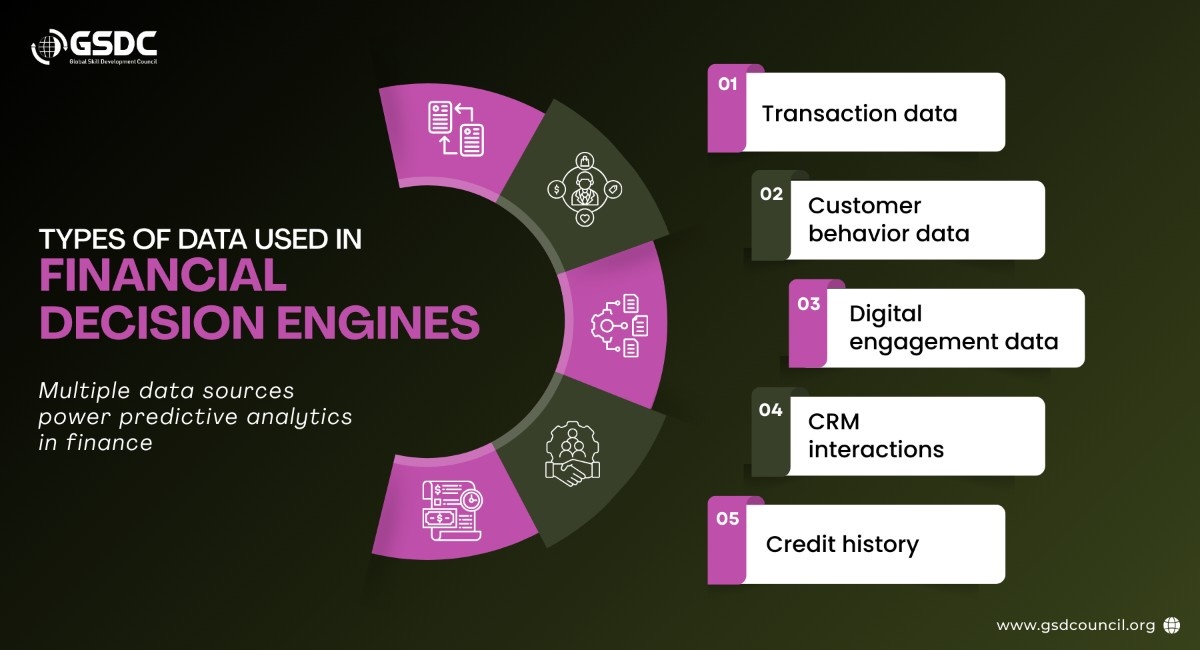

From Data to Decisions: The Role of Customer Data Features

At the core of any effective decision engine are customer data features. These are the data points and behavior signals used by models to make predictions, such as:

- Transaction patterns and frequency

- Changes in spending behavior

- Product usage history

- Digital engagement (app and online activity)

- Service interactions (support calls, complaints, resolution time)

The quality of these features directly affects the quality of predictions. Poorly integrated, outdated, or biased data leads to unreliable outcomes. Organizations that invest in data readiness -cleaning, integrating, and maintaining customer data -build a strong foundation for accurate and trustworthy decision engines.

This also strengthens CRM efforts. Predictive insights help teams deliver:

- More personalized communication

- Proactive customer support

- Better timing of offers

- Smarter prioritization of high-value or at-risk customers

In simple terms, better data leads to better decisions.

Business Impact: Where Decision Engines Deliver Value

Decision engines powered by predictive analytics enable financial institutions to transform data analytics in finance into real operational decisions.

1. Customer Experience and Retention

Predictive insights enable proactive service. Institutions can identify customers showing early signs of dissatisfaction or churn and intervene with timely support, personalized offers, or service improvements. This reduces attrition and strengthens long-term relationships.

2. Risk Management and Credit Decisions

A risk decision engine evaluates multiple data signals to estimate default probability, helping financial institutions balance risk management with financial inclusion.

3. Fraud Detection and Anomaly Monitoring

Using transaction monitoring and anomaly detection, real-time decision engines can flag suspicious financial activity instantly, preventing fraud and protecting customers.

4. Revenue Optimization

Targeted campaigns based on propensity scores improve conversion rates while lowering marketing spend. Teams can focus efforts on customers most likely to respond, driving efficient, customer-centric growth.

These outcomes demonstrate the broader benefits of AI in finance, including efficiency, risk reduction, and improved customer experiences.

How Propensity Models Are Built and Sustained

Implementing predictive decision engines requires a structured lifecycle supported by decision engine software and advanced data infrastructure.

- Data Preparation: Ensuring data is accurate, deduplicated, and compliant with privacy and regulatory standards

- Feature Engineering: Selecting meaningful attributes while removing sensitive or biased variables

- Model Training and Validation: Building predictive models using machine learning in financial services

- Deployment: Integrating models into operational systems where they can support real-time or near-real-time decisions

- Continuous Monitoring and Retraining: Regularly reviewing model performance and updating models as customer behavior, products, and market conditions evolve

This continuous improvement cycle ensures that decision engines remain relevant and aligned with real-world dynamics rather than becoming outdated or misleading.

Real-World Use Cases Across Financial Services

Decision engines and propensity models support multiple teams across financial organizations, including risk, operations, marketing, and customer experience.

Banking

- Credit scoring and loan approvals: AI improves risk assessment using behavioral and transaction data, enabling faster and fairer lending decisions.

- Personalized product offers: Banks recommend relevant products based on customer needs and behavior, improving conversion and satisfaction.

- Branch performance planning: Predictive insights help optimize staffing, operating hours, and resource allocation.

- Customer churn prediction: Early warning signals help banks retain customers through timely interventions.

Insurance

- Fraud detection: AI flags unusual claim patterns for faster fraud identification and review.

- Risk profiling and pricing: Insurers personalize premiums based on individual risk signals.

- Claims processing: Automated assessments speed up claim decisions and improve consistency.

These examples show how decision engines act as cross-functional enablers, improving decisions across the organization.

Key Challenges Leaders Must Address

While the benefits are compelling, adoption comes with important challenges:

- Data Integration: Combining data from multiple internal systems and external sources without compromising quality

- Privacy and Governance: Ensuring compliance with regulations and preventing biased or discriminatory outcomes

- Scalability: Designing platforms that can handle growing data volumes and seasonal demand

- Leadership Buy-In: Aligning stakeholders on investment, risk tolerance, and long-term value

- Cost of Continuous Improvement: Balancing retraining and infrastructure costs with measurable business impact

Overcoming these challenges requires not just technical capability, but strong governance, cross-functional collaboration, and leadership commitment.

A Leadership Lens: What Financial Leaders Should Do Next

Organizations that succeed with predictive decision engines typically:

- Build strong data foundations before scaling advanced AI models

- Establish clear governance and ethical AI guidelines

- Start with high-impact, well-defined use cases

- Measure success in terms of both business outcomes and customer trust

- Treat AI adoption as a long-term capability, not a one-off implementation

Decision engines and propensity prediction should be viewed as strategic enablers of customer-first, resilient financial services, not isolated technology initiatives.

Building AI Capabilities in Financial Services

As predictive analytics and AI decision engines reshape financial services, professionals need the skills to design and govern these technologies effectively. The Global Skill Development Council (GSDC) supports this shift through programs like the Certification in Generative AI in Finance and Banking, helping finance professionals understand how AI, data analytics, and intelligent decision systems are transforming modern financial operations.

Conclusion

Decision engines powered by propensity prediction represent a fundamental shift in how financial institutions operate. By leveraging customer data features and predictive analytics, organizations can move from reactive decision-making to a proactive, data-driven strategy.

The long-term value lies not only in efficiency and revenue growth, but in building more personalized, trustworthy, and responsive financial services. As predictive analytics continues to evolve, institutions that invest early in strong data foundations, governance frameworks, and leadership alignment will be best positioned to compete in the future of finance.

References:

Krishnan, G., Bhat, A. K., & Shah, J. (2025). Decision engine: Propensity prediction in the financial industry based on customer data features. Artificial Intelligence and Sustainable Innovation, 107–112. https://doi.org/10.1201/9781003731689-17

Related Certifications

Frequently Asked Questions

Stay up-to-date with the latest news, trends, and resources in GSDC

If you like this read then make sure to check out our previous blogs: Cracking Onboarding Challenges: Fresher Success Unveiled

Not sure which certification to pursue? Our advisors will help you decide!